Physitrack (PTRK): European Insurer Deal Extends MSK Reach - Research Note

Physitrack (PTRK) has signed an agreement with one of mainland Europe’s largest insurers to launch a consumer-facing MSK self-management and triage product. The first phase brings in €55k upfront and €24k ARR, with further rollout phases expected in Q4’25 and Q1’26.

The solution allows plan members to proactively screen and manage MSK conditions through Physitrack’s exercise library and engagement tools, escalating to physiotherapy when appropriate. This represents a clear step in expanding the Group’s distribution channels beyond healthcare providers into direct insurer-driven offerings.

The digital MSK market is large and growing, driven by rising MSK prevalence, aging populations, pressure on healthcare costs, and increased acceptance of digital triage and self-care tools.

Financially, the contract is modest. For comparison, Group ARR in Q2’25 stood at €13.2m, up 21% YoY. However, the strategic significance outweighs the numbers: the deal validates Physitrack’s ability to open new routes to market and demonstrates further scalability of its SaaS-led model.

Our take: The agreement is small in immediate value but important as a proof point. It strengthens Physitrack’s positioning in the MSK digital health market and underscores management’s focus on building high-margin, recurring revenue streams.

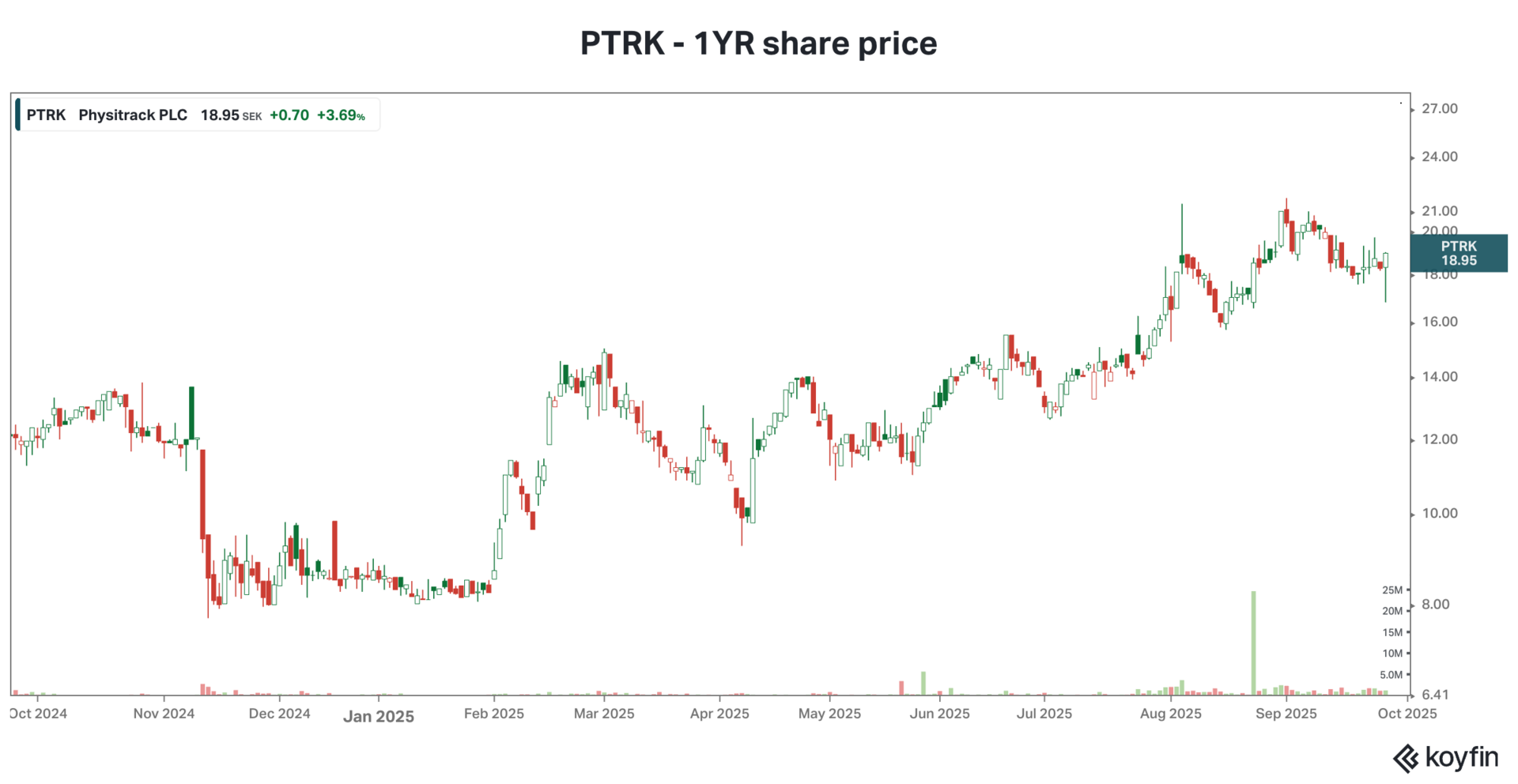

On valuation, we note that PTRK’s share price has eased somewhat after the sharp rebound that followed the resolution of the shareholder overhang. Importantly, no material negative news has emerged, and we see no reason the company will not continue to deliver rising earnings and materially improved cash flow in the coming quarters. In our view, this underpins a continued re-rating of the shares from currently depressed multiples. The current valuation multiples remain significantly below those of relevant Nordic SaaS peers, and we expect them to converge further. Our positive view on the share remains solid.