Idea note

This is an Idea note; It’s a collection of early signals – companies mentioned in fund letters, blogs, or by sharp investors online. Not a full pitch, just a starting point for ideas that might be worth a more in-depth look.

Coffee Stain Spin-off Creates Multiple Value Unlocking Opportunities for Embracer Group

Idea source: Lancelot

Embracer Group AB (EMBRAC) is a Swedish gaming conglomerate that operates in game development, publishing, and entertainment services across PC, console, and mobile platforms. It is listed on Nasdaq Stockholm and has operations in over 30 countries, managing premium intellectual property, including the rights to the Lord of the Rings.

Ticker: EMBRAC | Timeframe: 12-18 months | 💼 Special situation

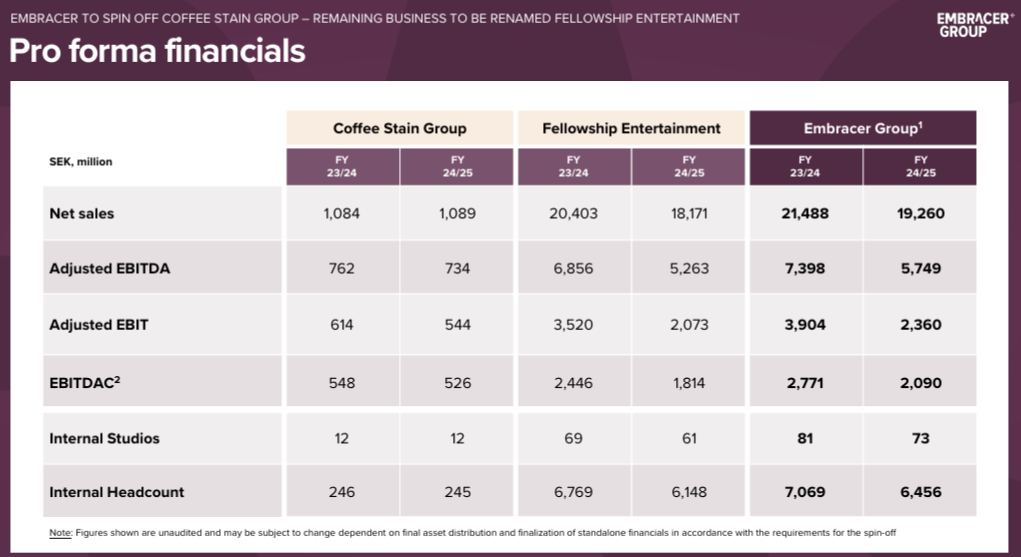

Lancelot Fonder believes that Embracer Group represents a compelling special situation investment despite weak near-term guidance due to limited major game releases. The fund identifies the upcoming Coffee Stain Group spin-off as a key value catalyst, noting the subsidiary’s strong operating margins exceeding 50% and expecting the separately listed entity to trade at 30-45 SEK per share. Lancelot argues that after adjusting for Coffee Stain’s value and Embracer’s net cash position of approximately 25 SEK per share, the remaining business trades at an exceptionally low valuation despite generating over 75% of total results. The fund sees the Lord of the Rings rights as Embracer’s most valuable asset, currently generating modest royalty income with significant upside potential.

Setup: Undervalued gaming conglomerate trading below sum-of-parts value due to market skepticism.

Latest Development: Coffee Stain spin-off announced for end of 2025, Fellowship Entertainment rebranding initiated.

Mispricing Reason: Market pessimism toward the gaming sector and a complex holding structure obscuring asset values.

Timing Catalyst: Multiple spin-offs creating pure-play investment opportunities with clearer value proposition.

Value Catalysts: Capital returns to shareholders, additional asset divestitures, strategic communication improvements.

Upside Potential: A sum-of-parts valuation suggests a 30-45 SEK Coffee Stain value, plus 25 SEK in net cash, creating a substantial value gap.

Key Risks: Gaming industry cyclicality and execution risks associated with corporate restructuring.

Disclaimer - Not Investment Advice

The content on Lind Research is for informational purposes only and should not be considered as investment advice financial advice. One should always consult a qualified professional before making any investment decisions. Investments carry risks, including the potential loss of capital. Lind Research and its authors bear no liability for decisions made based on the information provided here. All views are personal and not reflective of any company mentioned. Lind Research, it’s affilaites, personnel, clients and/or partners might hold investments in securites discussed.

By accessing Lind Research, you acknowledge and agree to this disclaimer.