What to Expect in the Report

Physitrack (PTRK) is scheduled to release its report for the second quarter of 2025 on July 24. In this note, we outline the key points we will focus on when reviewing the report.

Since our release of the investment case deep dive, see here, the share price has advanced around 20%. We do, however, view this as only the start of a longer revaluation journey that we envision over the coming years. For a full disclaimer, we are long (very long) in the shares of PTRK as a core portfolio holding.

We shy away from relying too much on quarterly misses or beats, which is a game of fools in our view. The value lies in understanding the economic reality and projecting that into the future, and buying that future when market expectations are low.

What we hope to see, however, is that the company is heading in the right direction with its current strategic initiatives and shareholder value optimization, as outlined in the investment case. Here are the focus areas for us when reading the Q2 report:

1 - Cost optimization

2 - Lifecare growth

3 - Reporting structure

4 - Cash flow focus

5 - Wellness deal and commentary

Let’s dig into it further.

1- Cost Optimization on the Way

We expect to see communication about the ongoing cost optimization programs. It’s likely that we will see NRI-related to cost cuts, which is all good in our view. A somewhat reduced headcount is what we expect to see.

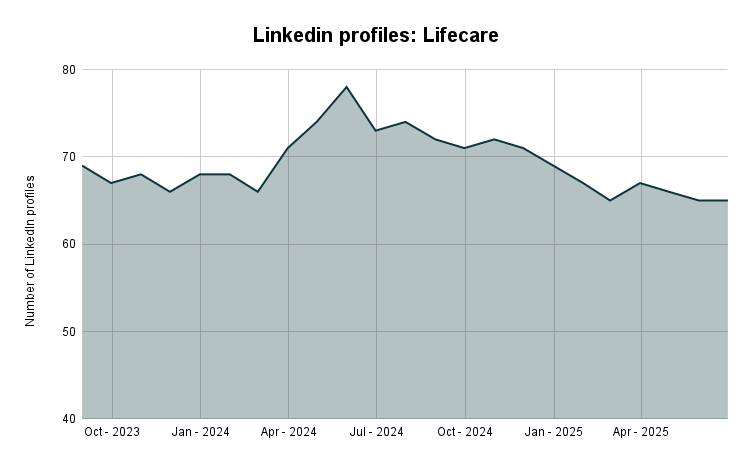

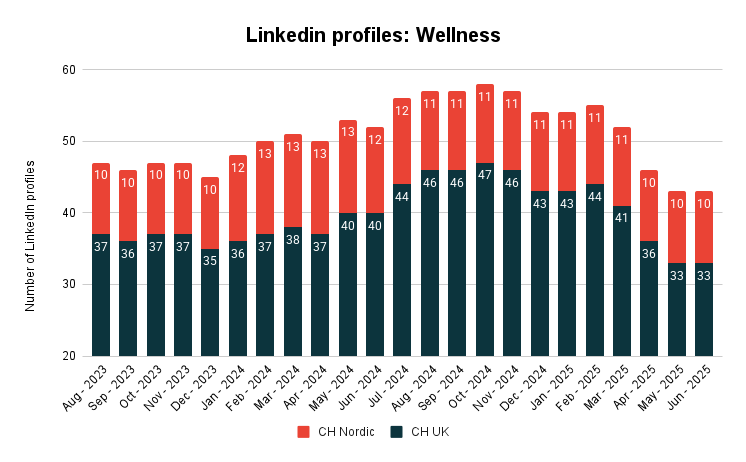

Looking at LinkedIn Data

A good way to gauge hiring activity is to monitor the LinkedIn profiles of Physitrack PLC and the various Champion Health companies. The LinkedIn profiles often do not accurately reflect the reported numbers, as some individuals working part-time or in consultancy roles may list their jobs on the profile. However, they are usually a good indicator of the hiring trend.

For Lifecare, we track the Physitrack PLC LinkedIn page. The number of linked profiles has steadily decreased, and for Q2, compared to the same period one year ago, it’s down approximately 13%.

For Wellness, we monitor Champion Health UK and Champion Health Nordic. There is also a separate LinkedIn page for Champion Health Plus, but we think it’s more or less the same as the UK profile page

Overall, it appears that cost measures within Wellness are underway, with a reduction in headcount. Compared to Q2 last year, the number of profiles has decreased by about 15%. There has been a clear reduction during the quarter, with a decrease of approximately 19% compared to Q1'25.

We believe the LinkedIn numbers indicate that the cost programs are underway, and we expect to see either direct effects in the report or work related to the development.

2 - Lifecare Continues to Grow

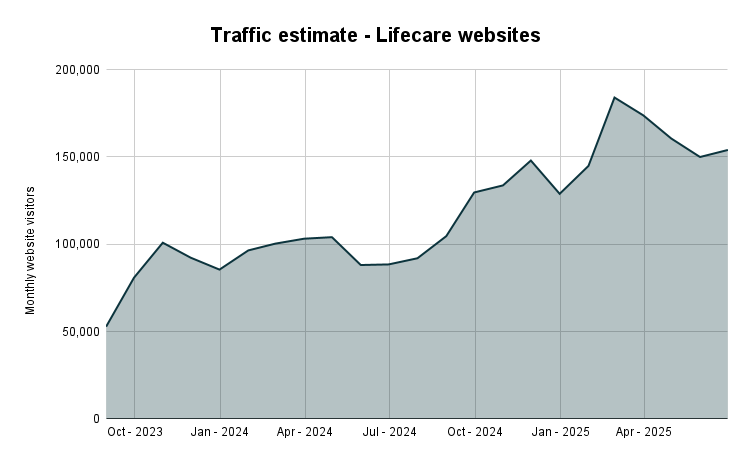

A core part of our thesis in Physitrack is the strong growth engine and stability of Lifecare. Management has mentioned multiple times their work with SEO and product-led growth. Therefore, we track estimates of website visitors for the different websites in the Lifecare portfolio, which include: physitrack.com, physicourses.com, physiapp.com, physidata.com.

The estimated website visitors are up close to 65% on a year-over-year basis, but down about 11% compared to Q1. Compared to Q2 '24, it appears that there will be steady and healthy growth.

Lifecare Expectations

Our full-year estimates for Lifecare are based on an uptake of approximately 7%. We expect to see a similar trend in the Q2 report. According to this Redeye1 report, there should have been price increases in May, which should have helped the ARPU during Q2. We hope to see underlying profitability in line with our full-year projections, where we expect adjusted EBIT margins of around 18%.

3 - Reporting Structure

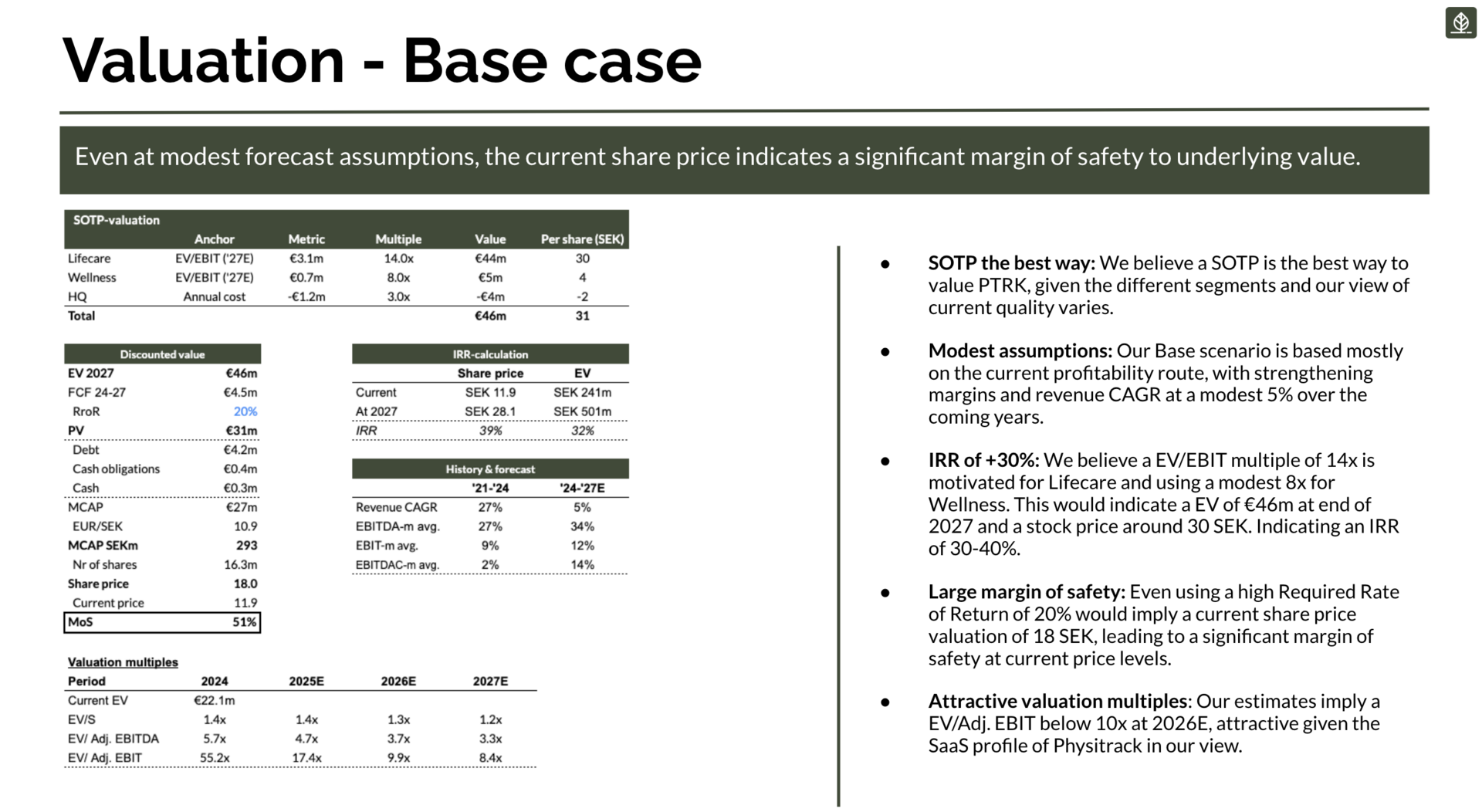

A central part of our thesis for Physitrack is that Lifecare is a hidden value, and that the current reporting format makes it difficult to understand the quality of the Lifecare business. We firmly believe that the Lifecare segment, on its own, more than fills the current market value and even exceeds it. Here is a brief reminder of our SOTP valuation:

We have shared our thoughts with the management team and expect to see clear improvements in the report. We saw some initial progress in the Q1 filing with SaaS KPIs, so everything appears to be heading in the correct direction.

3 - Cash Flow Focus

We hope that the new reporting will focus primarily on cash flow measures rather than EBITDA. As Physitrack has a considerable amount of CAPEX related to development, focusing on EBITDA is not proper.

In discussions with management, they have been positive about focusing more on cash flow (or EBITDA-CAPEX) and may also consider a return metric, such as ROCE/ROIC. We will see if the company follows through on that, but it would be a clear positive development, in our opinion.

Summary

To summarize, we are not overly concerned about short-term development as long as the company is moving in the correct direction. We expect additional costs, but as these are driven by layoffs and cost-cutting measures, we view them as positive. What is crucial is to see steps taken to focus on cash flow, return metrics, and ensuring the Lifecare value holds up, as well as more shareholder-friendly reporting.

Disclaimer - Not Investment Advice

The content on Lind Research is for informational purposes only and should not be considered as investment advice financial advice. One should always consult a qualified professional before making any investment decisions. Investments carry risks, including the potential loss of capital. Lind Research and its authors bear no liability for decisions made based on the information provided here. All views are personal and not reflective of any company mentioned. Lind Research, it’s affilaites, personnel, clients and/or partners might hold investments in securites discussed.

By accessing Lind Research, you acknowledge and agree to this disclaimer.