Idea note

This is an Idea note; It’s a collection of early signals – companies mentioned in fund letters, blogs, or by sharp investors online. Not a full pitch, just a starting point for ideas that might be worth a more in-depth look.

Undervalued Kitchen Giant Poised for Operational Transformation

Idea source: Adrigo

Price 5.3 SEK (2025-07-17)

Nobia AB is one of Europe’s largest kitchen manufacturers, operating through 10 strong local brands in the Nordic region and the UK. The company designs, manufactures, and sells kitchen solutions with an annual revenue of SEK 10.4 billion across consumer, trade, and project segments

Ticker: NOBI | Timeframe: 18-24 months | 🔁 Turnaround

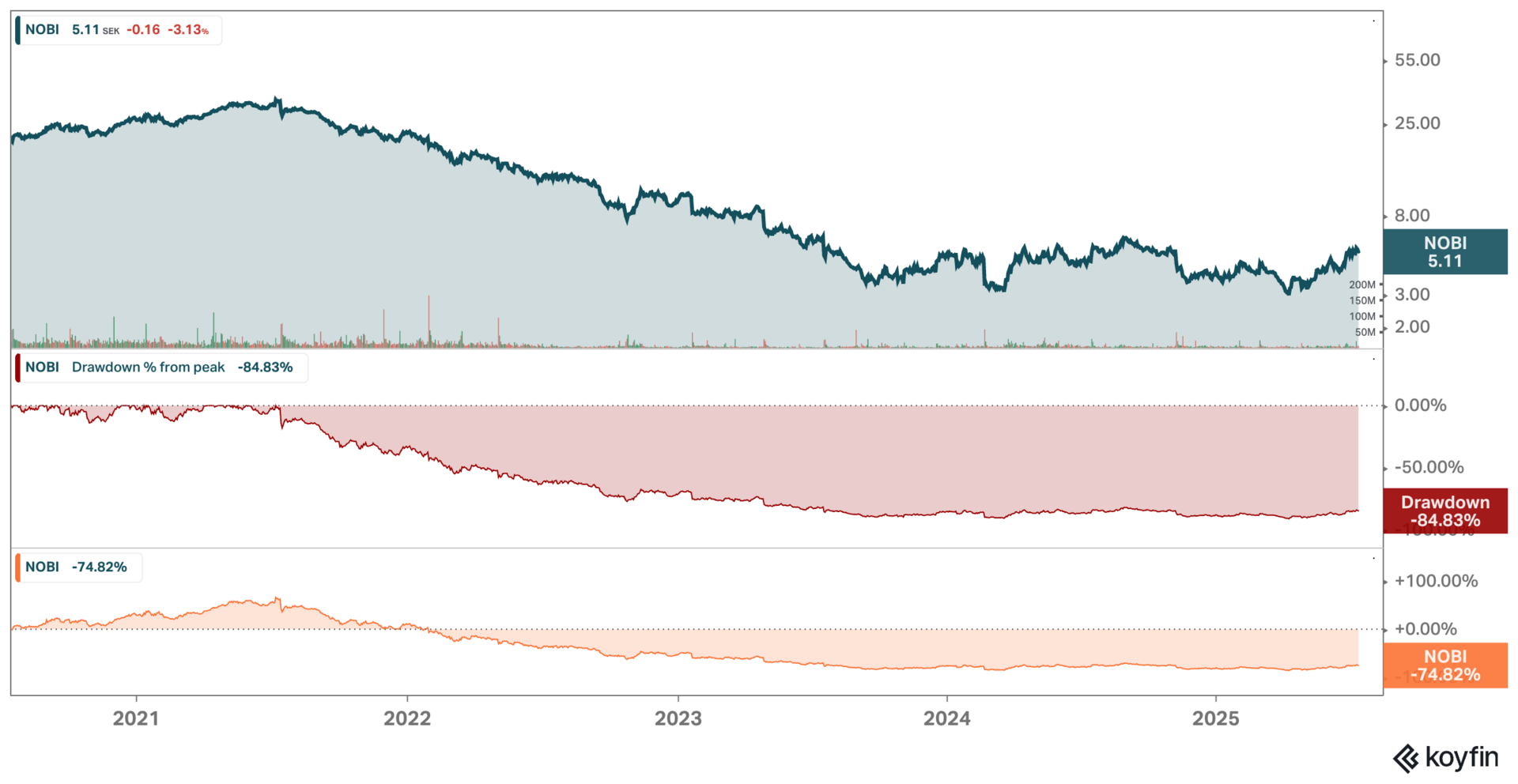

Adrigo believes Nobia presents a compelling turnaround opportunity following a steep four-year share price drop, with it’s market cap going from SEK 12 billion to SEK 3.3 billion. The fund sees the kitchen market as having bottomed out, especially in the consumer segment, which is recovering due to Swedish tax relief measures and decreasing interest rates. Adrigo anticipates that the completion of Nobia’s SEK 3.7 billion automated factory in Jönköping will significantly boost margins by reducing production costs by 30%, while strong cash flows from improved earnings and low tax payments should quickly lower net debt and the market’s risk premium.

Setup: Distressed valuation after 75% market cap decline despite rights issue strengthening balance sheet.

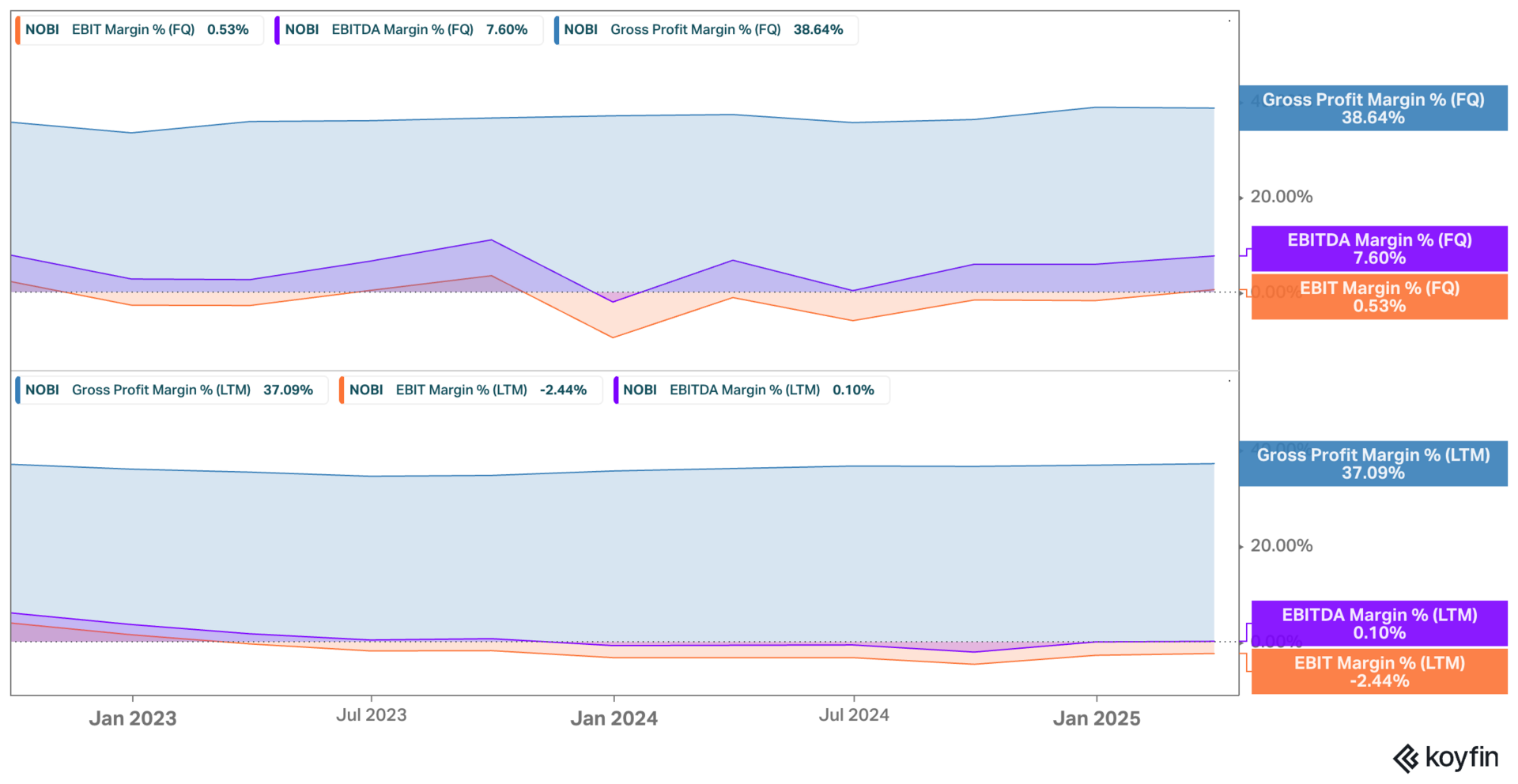

Latest Development: Q1 2025 showed positive adjusted EBIT turnaround with 38.6% gross margin (highest since 2018) and significant Nordic profitability improvement.

Reason for Mispricing: Market pessimism over prolonged project market weakness obscures the benefits of consumer recovery and factory transformation.

Timing: The Jönköping factory is ramping up production, with gradual customer shipments starting in May 2025.

Value Catalysts: Factory capacity utilization, margin expansion, debt reduction, and project market recovery.

Risks: Delayed housing market recovery, UK market deterioration, factory ramp-up execution challenges

Disclaimer - Not Investment Advice

The content on Lind Research is for informational purposes only and should not be considered as investment advice financial advice. One should always consult a qualified professional before making any investment decisions. Investments carry risks, including the potential loss of capital. Lind Research and its authors bear no liability for decisions made based on the information provided here. All views are personal and not reflective of any company mentioned. Lind Research, it’s affilaites, personnel, clients and/or partners might hold investments in securites discussed.

By accessing Lind Research, you acknowledge and agree to this disclaimer.